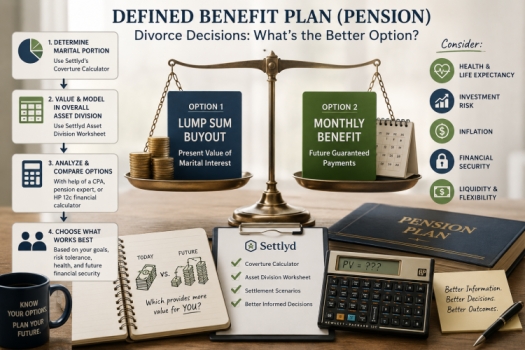

Defined Benefit Plans in Divorce: Lump Sum Buyout or Monthly Benefit?

Defined benefit plans — commonly referred to as pensions — are often among the most valuable assets in a divorce case. Unlike a 401(k) or IRA with a readily identifiable balance, pensions require additional analysis to determine both the marital portion and the best method of division.

In some cases, one spouse prefers to “buy out” the other spouse’s interest by determining the present value of the marital portion of the pension and including that value in the overall equitable distribution. In other situations, the parties may prefer to divide the future monthly benefit itself through a deferred distribution and QDRO approach.

So how can attorneys and clients evaluate which option may work best?

Using the tools available in Settlyd Family Law Software, practitioners can model and compare these scenarios more effectively.

The first step is determining the marital portion of the pension using Settlyd’s coverture calculator. This helps establish what percentage of the pension was earned during the marriage and therefore subject to equitable division.

From there, the value can be incorporated directly into the Settlyd Asset Division Worksheet, allowing attorneys to see how a pension buyout impacts the entire marital estate. For example, one spouse may retain the pension while the other receives additional equity in the home, retirement accounts, or other assets to offset the pension’s present value.

But determining whether a lump-sum buyout is preferable to retaining future monthly benefits often requires additional financial analysis. This is where collaboration with a CPA, pension expert, or even a classic financial tool such as the HP 12C calculator can be valuable. By applying present value calculations, discount rates, mortality assumptions, and expected retirement dates, the parties can compare the long-term value of future pension payments against a current offset today.

There is no universal answer. A younger spouse may prefer a clean buyout and immediate certainty. Another party may value the long-term security of guaranteed monthly payments. Health considerations, inflation, life expectancy, investment risk, and liquidity all play important roles.

The ability to model these alternatives clearly is critical. Settlyd’s calculators and asset division tools help attorneys create and evaluate multiple settlement scenarios so clients can make informed decisions tailored to their financial goals and risk tolerance.

Guy Vitetta, Charleston SC